](https://file-host.link/website/unleashx-1r3z1u/assets/blog-images/b57b8f6c-ae2f-47d4-812f-4a674582445b/1774861842874037_2dad0b17e0664c0e9c4d1afc4d7958f7/360.webp)

Introduction

Voice AI IVR integration with mortgage servicing platforms is technically demanding by nature. It operates at the intersection of legacy telephony infrastructure, regulated loan servicing systems (LOS/MSP/CRM), and AI models that must work within strict compliance guardrails.

This integration requires coordination across IT teams (telephony/API owners), compliance officers, and AI vendor support, it is not a self-serve configuration task.

Poor integration carries real consequences:

- Broken call flows mid-borrower interaction

- Data failing to write back to the servicing platform

- Compliance exposure from unguarded AI responses

- Low borrower adoption that undermines ROI

This guide walks through the integration process from prerequisites through step-by-step phases, validation, and common failure patterns so mortgage servicers can deploy Voice AI IVR that holds up in production.

Key Takeaways

- Voice AI IVR integration is a multi-phase technical project requiring telephony, API, compliance, and dialogue configuration work

- Confirm API availability for your LOS/MSP/CRM, telephony compatibility, and regulatory compliance requirements before starting

- Expect five sequential phases: scoping, telephony setup, API connections, AI dialogue configuration, and pilot testing each with its own dependencies

- Before deployment, validate with borrower flow testing, load testing, and a full compliance review

- The most common failure points are data sync delays, authentication gaps, and the AI failing to hand off calls cleanly when borrower queries get complex

Prerequisites Before You Integrate Voice AI with Your Mortgage Servicing Platform

Integration cannot begin until foundational system readiness is confirmed. Skipping this phase leads to mid-project blockers and costly rework.

System and API Readiness

Verify that your mortgage servicing platform (MSP, LOS, or CRM) provides the APIs or webhooks needed for real-time read/write operations. The system must support:

- Loan status and payment history

- Escrow data

- Borrower identity verification

- Document status tracking

Older systems may require middleware or an integration hub. Major platforms have moved quickly here: Black Knight launched its Developer Portal in January 2023, offering APIs, web services, and webhooks across the mortgage life cycle. ICE Mortgage Technology offers Encompass Developer Connect with REST APIs and premium Webhook Custom Auth APIs.

For legacy environments, middleware is no longer optional, the Integration Platform as a Service (iPaaS) market grew 23.4% to $8.5 billion (approximately ₹70,600 crore) in 2024, making middleware the standard bridge between older systems and modern APIs.

API readiness covers your data layer but the voice path needs its own check. Confirm telephony layer compatibility by determining whether your current setup uses:

- SIP trunking

- Cloud-based VoIP

- Legacy PBX

The Voice AI platform must connect natively or through carrier-side configuration changes. Despite rapid cloud migration, Gartner data from 2021 showed 71% of pan-India business telephony users were still running on-premises telephony.

Compliance and Data Governance Groundwork

Identify the regulatory obligations governing Voice AI behavior in your state(s):

- TRID disclosure requirements

- GLBA data handling rules

- FDCPA collection communication rules

- TCPA consent for outbound AI calls

- State-specific recording consent laws (one-party vs. two-party consent)

The TCPA item above carries particular weight for outbound AI calling. In February 2024, the FCC issued a Declaratory Ruling confirming that TCPA restrictions on "artificial or prerecorded voice" cover current AI-generated voice technologies. Prior express consent is required before any outbound AI voice call.

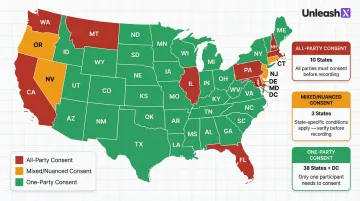

State call recording consent laws vary significantly:

| Consent Type | States | Key Requirements |

|---|---|---|

| All-Party (10 states) | CA, FL, IL, MD, MA, MT, NH, PA, WA, DE | Requires consent from all parties |

| Mixed/Nuanced | CT, NV, OR | Different rules for phone vs. in-person |

| One-Party (38 states + DC) | TX, NY, GA, OH, etc. | Only one person needs to consent |

Establish data governance rules before integration begins:

- What borrower data can the AI access?

- How will data be stored and encrypted?

- What are retention and audit log requirements?

Hard non-negotiables: Do not proceed if your LOS/MSP has no API layer, if compliance review hasn't been initiated, or if the AI vendor cannot demonstrate mortgage-specific compliance guardrails in an existing production deployment.

How to Integrate Voice AI IVR with Mortgage Servicing Platforms

Integration follows a defined sequence. Compressing phases particularly skipping compliance configuration or piloting at full scale immediately is the most common cause of failed deployments. Each phase builds on the last.

Phase 1: Scoping and Architecture Design

Define the primary use case for Phase 1. Typically one of:

- Inbound balance/payment inquiries

- Outbound delinquency outreach

- Loan status updates

Resist integrating all use cases simultaneously. Scope tightly to contain risk and measure outcomes clearly.

Map the call routing architecture:

- Which inbound phone queues or outbound dialing campaigns will route to the AI?

- What does the escalation path to a human agent look like?

- How will context (loan number, intent, prior interaction history) be passed during transfers?

Phase 2: Telephony Layer Connection

Connect the Voice AI platform to your telephony infrastructure:

- Configure SIP trunk connections or cloud telephony APIs (such as Twilio)

- Assign DIDs (direct inward dial numbers) or route through your existing IVR entry point

- Verify call recording is enabled for compliance logging

Test call quality at this stage independently of AI functionality. Confirm latency is within acceptable thresholds. Cisco's UCCE design guide warns that Voice AI requires round-trip latencies under 50ms, with disruptions occurring past 150ms.

ITU-T G.114 standards allow up to 150ms of one-way delay for human-to-human calls. Voice AI systems face tighter constraints: they must execute Speech-to-Text, Natural Language Understanding, API data dips, and Text-to-Speech within that same window.

Verify audio fidelity is acceptable and failover routing to human agents works correctly if the AI platform becomes unavailable.

Phase 3: Mortgage Servicing Platform API Integration

Connect the Voice AI's orchestration layer to your LOS/MSP/CRM via APIs or middleware. Map specific data fields the AI will need to:

Read:

- Loan status

- Next payment date

- Escrow balance

- Outstanding conditions

Write:

- Interaction outcome

- Payment confirmation

- Callback scheduling

Test data write-back in a sandbox environment with masked or synthetic borrower data before any live traffic. Confirm that AI-initiated actions (marking a payment intent, logging a hardship inquiry) actually update the servicing system records in real time, not in batch.

ICE Encompass restricts applications to a maximum of 25 Webhook Subscriptions per lender, requiring careful subscription management and caching. Plan your subscription allocation before moving into dialogue configuration API constraints at this layer directly affect which events your AI can monitor and act on.

Phase 4: AI Dialogue and Compliance Configuration

Configure the Voice AI's dialogue flows for each use case:

- Define intents (payment inquiry, loan status, hardship request, refinance inquiry)

- Set required disclosure language at specific conversation points

- Configure prohibited phrases

- Establish confidence thresholds that trigger human transfer

Platforms with pre-built mortgage-specific dialogue templates reduce configuration time significantly. UnleashX, for example, provides production-ready AI employee templates that connect to existing servicing systems without custom development for each integration point.

Set up voice biometric or alternative authentication flows if applicable. Define how the AI will verify borrower identity (loan number + last four of SSN + voice passphrase) before accessing or acting on account data. Confirm this meets your security policy.

Compliance note: FDCPA §1692e(11) mandates that debt collectors disclose in the initial oral communication that they are attempting to collect a debt. Voice AI systems must deliver these disclosures automatically and accurately configure and test this before any live traffic reaches the system.

Phase 5: Internal Pilot Before Go-Live

Route a narrow, controlled subset of traffic to the Voice AI first. Examples:

- After-hours inbound calls for a single loan portfolio

- A defined outbound campaign

Involve 3–5 experienced servicing staff in reviewing interaction transcripts and escalation quality daily during the pilot window.

End-to-end, most integrations run 8–12 weeks from scoping through telephony setup, API configuration, dialogue build, and controlled pilot before full rollout.

Post-Integration Testing and Validation

Failures discovered after borrower-facing go-live carry compliance, reputational, and legal risk. Validate the integration fully before production deployment, there is no safe shortcut in a regulated lending environment.

Functional and Compliance Testing

Run structured borrower flow simulations covering the most common interaction paths:

- Payment inquiry

- Status check

- Hardship trigger

- Escalation request

Verify that:

- The AI retrieves accurate data from the servicing platform

- Disclosures are delivered at the correct conversation point

- Escalation to a human agent passes full interaction context cleanly

Conduct a compliance review of a sample set of simulated transcripts with your legal/compliance team before go-live. Confirm required disclosures are present, prohibited language is absent, and the AI does not make statements that could be construed as legal or financial advice beyond its configured scope.

Load and Continuity Testing

Once functional and compliance checks pass, confirm the system holds up under real-world demand. Simulate concurrent call volumes for peak scenarios, including:

- Rate-drop spikes driving sudden inquiry surges

- Payment-due-date rushes with high simultaneous inbound volume

- Failover activation when the AI platform becomes unavailable

Confirm the AI maintains response quality and latency without degrading across each condition. Also verify that failover routes borrowers cleanly to human agents or a backup IVR menu not to a dead end.

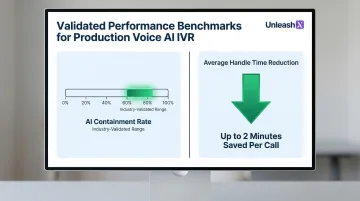

Use published benchmarks as your validation targets: well-integrated AI IVR systems achieve 60% to 85% containment rates and can reduce Average Handle Time (AHT) by up to 2 minutes. If load testing results fall significantly short, investigate latency bottlenecks at the API layer before go-live.

Common Integration Problems and How to Fix Them

The following issues appear consistently across Voice AI IVR integrations with mortgage servicing platforms. Most are preventable but frequently appear when teams skip the prerequisites phase.

Data Not Writing Back to the Servicing Platform

The Voice AI confirms an action to the borrower logging a payment intent or scheduling a callback but the outcome never appears in the LOS/MSP record. Loan officers have no visibility into what was promised.

Root cause: The connection was configured for read-only access to fetch data. Write-back endpoints were never authenticated or tested.

How to fix it:

- Audit API permission scopes for every data write the AI is expected to perform

- Test each write action explicitly in the sandbox environment

- Confirm the servicing system record reflects the change before go-live

AI Escalating Too Frequently (or Not Enough)

The Voice AI either overwhelms the call center by transferring too many calls, or handles complex hardship and modification requests that should always go to a specialist.

Root cause: Confidence thresholds and escalation intent triggers were set too conservatively or too liberally during dialogue configuration, without testing against real borrower query patterns.

How to fix it:

- Review the first two weeks of pilot transcripts for phrases triggering (or failing to trigger) escalation

- Recalibrate thresholds based on actual query distribution not assumptions from initial configuration

Compliance Disclosures Being Skipped or Misplaced

Required disclosures call recording notice, AI agent identification, FDCPA-mandated language for collection contacts are absent from certain interaction paths or delivered at the wrong point in the conversation.

Root cause: Disclosure logic was configured only for the primary happy-path flow, never tested against branch paths triggered by borrower interruptions or mid-call topic changes.

How to fix it:

- Map every possible conversation branch before compliance testing begins

- Validate disclosure delivery across each path not just the expected flow

- Configure disclosures as mandatory gates that fire regardless of conversation path, not as optional dialogue nodes

Pro Tips for a Successful Voice AI IVR Integration

Involve compliance and legal from Phase 1, not as a final review gate. Decisions made in scoping what data the AI can access, what it can say, how it handles collection contacts are compliance decisions. Late-stage compliance review forces expensive rework of already-built dialogue flows.

Treat the integration as an iterative system, not a one-time project. Plan for a 90-day optimization window post-launch where you:

- Review transcripts weekly

- Adjust escalation thresholds

- Refine dialogue flows based on real borrower behaviour

- Layer in additional use cases (adding outbound delinquency outreach after inbound stabilises)

Platforms that combine Human-in-Loop design with continuous compliance monitoring, such as UnleashX, make this ongoing governance easier to manage at scale without adding manual oversight overhead.

Document and sign off on every integration component before go-live. Maintain a record of:

- API endpoints configured

- Data fields mapped

- Compliance disclosures approved

- Dialogue flows reviewed

- Pilot results

This documentation becomes your evidence pack for regulators and internal auditors.

Frequently Asked Questions

How does AI fit Indian mortgage lenders, HFCs, and NBFCs?

Indian housing finance companies (HDFC Ltd, LIC HF, PNB HF) and NBFCs use AI for application triage, document verification (Aadhaar / PAN / income proofs), property valuation analytics, and customer follow-up across English, Hindi, and regional languages. RBI and NHB guidelines on IT outsourcing govern deployments, so providers maintain audit trails for every decision.

Which Indian regulations apply to AI in mortgage and home loan workflows?

RBI master directions for HFCs and NBFCs, NHB regulations, DPDP 2023 for personal data, and IT Act provisions on electronic records all apply. KYC for housing loans is governed by RBI's master KYC direction and CKYC. Production AI systems for lending must keep model decision logs, fair-lending audit trails, and adverse-action reasons retrievable on demand.

How do Indian borrowers prefer to interact with mortgage lenders?

WhatsApp and voice calls dominate Indian borrower engagement. SMS-based status updates, regional-language voice IVRs, and human handoff inside the same WhatsApp thread are standard expectations. Lenders combining voice AI for first-touch with branch RM follow-up see higher application completion rates compared with email-led journeys typical in Western markets.

How does Voice AI connect to existing mortgage LOS or CRM systems?

The connection is made via REST APIs or middleware integration hubs that allow the AI to read loan data in real time and write interaction outcomes (payment intents, callback schedules, hardship flags) back to the servicing record.

What happens when a borrower asks something the Voice AI cannot handle?

Confidence thresholds detect out-of-scope or high-complexity queries and trigger a warm transfer to a human agent. Full conversation context passes with the transfer, so the borrower doesn't have to repeat themselves.

How do mortgage servicers measure ROI after Voice AI IVR integration?

Common ROI metrics include:

- AI containment rate : calls resolved without human transfer

- Average handle time reduction

- Cost per interaction

- Borrower satisfaction scores

- Promise-to-pay rate and right-party contact rate (outbound campaigns)

Want to see how UnleashX AI Employees can transform your business? Visit UnleashX to explore the full platform and book a personalized demo.