Introduction

Banks face a persistent operational paradox: despite decades of digital investment, productivity has declined by 0.3% annually since 2010. While front-end systems have been modernized, back-office workflows remain burdened by manual handoffs, siloed systems, and legacy processes. Between 60% and 70% of banking employee time is consumed by internal coordination and data updates rather than customer-facing work. Traditional automation tools like RPA have proven insufficient McKinsey estimates 30-50% of RPA implementations fail to deliver expected ROI due to fragility and maintenance overheads.

Where RPA breaks down, agentic AI picks up. Unlike chatbots that respond to prompts or RPA bots that follow rigid scripts, agentic AI systems reason, plan, and act across multi-step banking workflows without constant human direction. They handle the exceptions and edge cases that previously required escalation like loan processing discrepancies, compliance flag reviews, cross-system reconciliations.

The result is a shift from brittle task automation to systems that actually complete work. What that means for banking operations and how institutions can move past pilot projects into measurable impact is what this article addresses.

Key Takeaways

- Agentic AI plans and executes multi-step banking workflows covering everything from KYC to fraud detection without constant human prompting

- Key transformation areas: customer onboarding (reducing timelines from 95 days to hours), fraud prevention, credit assessment, and compliance documentation

- Deploying narrow point solutions rather than redesigning end-to-end domains is where most bank AI initiatives stall

- UnleashX AI employees go live in 45 minutes, connect across 200+ tools, and maintain 98% accuracy with built-in compliance monitoring

What Makes Agentic AI Different from Traditional Banking Automation

The Evolution Beyond RPA and Gen AI

Traditional automation approaches each fail in distinct ways. RPA automates fixed, deterministic steps by following UI-level scripts when an interface changes, the bot breaks. Generative AI creates content reactively from prompts but requires human orchestration for every task.

Agentic AI addresses both gaps. It combines perception (reading documents, system inputs, customer queries), reasoning (evaluating options and risk), action (executing tasks across tools and APIs), and memory (learning from context across workflows) into autonomous, goal-oriented execution.

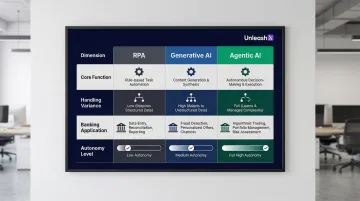

| Capability | RPA | Generative AI | Agentic AI |

|---|---|---|---|

| Core Function | Follows deterministic, UI-based scripts | Creates content reactively from prompts | Plans, decides, and executes multi-step workflows autonomously |

| Handling Variance | Breaks when UI or data formats change | Adapts to unstructured data but needs human orchestration | Uses semantic understanding to adapt to real-time changes |

| Banking Application | Simple data entry, screen scraping | Drafting credit memos, summarizing documents | End-to-end KYC orchestration, autonomous fraud investigation |

| Autonomy Level | None (strictly rule-based) | Low (human-prompted copilot) | High (goal-oriented with human-in-the-loop for exceptions) |

Why Banking Operations Are Ideal for Agentic AI

Between 50% and 60% of bank full-time equivalents are tied to service operations and task delivery, making operations the primary cost center and transformation opportunity. The scale of this opportunity is substantialMcKinsey estimates generative AI could add $200-$340 billion (approximately ₹2,822,000 crore) in annual value across pan-India banking, equivalent to 9-15% of operating profits.

Multi-Agent Orchestration for Complex Processes

Capturing that value requires more than faster automation, it requires systems that can coordinate across departments. Agentic AI introduces multi-agent orchestration where specialized agents work like a coordinated team: one extracts data from documents, another checks compliance, a third routes for approval all passing context seamlessly.

Banking processes routinely cross four or more departments. A single loan application involves credit assessment, fraud screening, compliance verification, and document management. Multi-agent systems handle these handoffs autonomously, cutting the back-and-forth that slows decisions by days.

Unlike RPA, which failed when it couldn't automate the full scope of a role, agentic AI handles the "long tail" of exceptions. When a credit application includes unusual income documentation or identity verification requires additional checks, agentic systems reason through the exception, gather additional data, and escalate only when human judgment is truly needed less than 15-20% of cases.

High-Impact Use Cases of Agentic AI in Banking Operations

These are areas where agentic AI is already delivering measurable impact on speed, cost, and accuracy through pilots and production deployments.

Customer Onboarding and KYC

Manual KYC processes drain resources corporate KYC reviews average ₹2.2 lakh (≈ $2,598)per case and take approximately 95 days, and 70% of financial institutions report losing clients due to slow onboarding.

Agentic AI handles the end-to-end workflow autonomously:

- Ingests documents from websites and regulatory filings

- Verifies identity and runs eligibility checks

- Screens for politically exposed persons (PEP), sanctions, and adverse media

- Routes completed files for human review or approval

One pan-India bank deploying an "agentic AI factory" with 10 specialized agent squads achieved 200-2,000% productivity gains. Data extraction agents structure initial KYC files, validation agents cross-reference government registers, screening agents perform compliance checks, orchestration agents compile consolidated reports, and QA agents ensure quality standards all autonomously. This reduces onboarding time from days to hours while freeing staff for exception handling and customer engagement.

Fraud Detection and Financial Crime Prevention

[$33.83 billion (approximately ₹280,800 crore)aud losses reached ₹280,789 crore (≈ $33.83 billion) in 2023](https://nilsonreport.com/articles/card-fraud-losses-worldwide-in-20$40 billion (approximately ₹332,000 crore)Deloitte projecting US fraud losses alone could hit ₹332,000 crore (≈ $40 billion) by 2027 as AI-enabled fraud tactics grow more sophisticated.

Agentic AI shifts the response from reactive alerts to proactive orchestration:

- Continuously monitors transaction patterns across accounts

- Cross-references signals from multiple data sources simultaneously

- Initiates investigation workflows without waiting for human triggers

- Adjusts detection models as fraud tactics change

This cuts false-positive rates that plague traditional rule-based systems while surfacing sophisticated fraud patterns earlier in the chain.

Credit Assessment and Loan Processing

McKinsey reports that multi-agent systems preparing credit memos yield 20-60% productivity gains and approximately 30% faster decision-making. AI agents gather applicant data, pull credit signals, generate assessment summaries, flag anomalies, and route cases for human review cutting timelines and improving decision consistency. In one case study, intelligent automation reduced loan processing times by 50% while achieving a 90% transaction success rate.

Regulatory Compliance and Risk Management

Agentic AI assists with risk and control self-assessments (RCSAs), control documentation, model reviews, and audit preparation by autonomously gathering data, structuring findings, and surfacing exceptions. Up to 85% of effort in compliance operations consists of clerical work and data gathering rather than risk judgment.

Agentic systems automate the data-heavy groundwork so compliance teams can focus where their judgment actually matters:

- Extract data from profit-and-loss statements, balance sheets, and company filings

- Identify ultimate beneficial owners across complex ownership structures

- Structure findings and flag anomalies for human review

The result: compliance teams spend their time on risk decisions, not data collection.

Customer-Facing Financial Assistance

Traditional digital self-service struggles only 14% of customer service issues are fully resolved in self-service, and 74% of consumers prefer human agents due to chatbot frustrations. Agentic AI handles complex requests dispute resolution, product queries, account changes by retrieving information across systems, initiating workflows, and escalating to humans when needed, all within a single interaction. NatWest's AI-powered assistant Cora handled over 11 million customer interactions in 2024, demonstrating the capacity for high-volume frontline engagement.

How Agentic AI Transforms the Back Office

The back office is where agentic AI delivers the most immediate and substantial impact. It's where the most labor-intensive, document-heavy, judgment-requiring tasks live and where AI can now operate under supervision at scale.

Connecting Front-End Intent to Back-End Fulfillment

Agentic back-office systems function as "connective tissue," linking customer intent with compliance controls, risk evaluation, and fulfillment into a single connected workflow rather than siloed handoffs.

For loan origination, this changes throughput dramatically. Instead of applications sitting in queues between credit analysis, compliance review, and documentation teams, agentic systems orchestrate all steps simultaneously reducing approval timelines by 30% or more.

Evaluation-Driven Development for Regulated Environments

Banks need assurance that agentic AI outputs are accurate, auditable, and consistent. Evaluation-Driven Development (EDD) has become the go-to methodology for LLM agents, where evaluation means applying specific criteria to observed outcomes to judge acceptability relative to stated objectives. This gives both internal teams and regulators confidence in system reliability over time, ensuring that autonomous decisions meet model risk management requirements.

Full-Stack AI Employees vs. Point Solutions

Full-stack AI employees go beyond task-specific bots by orchestrating workflows across 200+ tools with consistent, production-ready performance. Platforms like UnleashX deploy AI employees that handle lead follow-up, CRM updates, and customer re-engagement autonomously. Core performance benchmarks include:

- 98% accuracy across voice, chat, and task execution

- <700ms latency for real-time customer interactions

- Built-in compliance monitoring with full audit trails

- Reasoning through exceptions rather than halting on edge cases

This allows banking operations teams to deploy agentic capability without building infrastructure from scratch.

UnleashX's Loan Eligibility & Application Support Agent, for instance, handles customer onboarding end-to-end:

- Explains loan options and performs instant eligibility checks

- Collects application details and guides customers through each step

- Shares document requirements and provides live status updates

- Integrates with CRM systems while maintaining compliance with RBI guidelines and DPDP requirements

This autonomous orchestration frees human staff for higher-value judgment work and complex exception handling.

The Human-in-the-Loop: Why Oversight Still Matters in AI-Driven Banking

Human-in-the-loop isn't a limitation on agentic AI, it's a design principle. Well-architected systems escalate exceptions, flag low-confidence decisions, and maintain complete audit trails, giving managers full control without requiring them to supervise every transaction.

Regulatory and Model Risk Management Requirements

Banks operate under strict model risk management frameworks across every major jurisdiction:

- US: The Federal Reserve's SR 11-7 mandates rigorous model validation, effective challenge by objective parties, and comprehensive model inventories.

- Europe: The EBA's mapping of the EU AI Act to banking classifies AI systems used for creditworthiness evaluation as "high-risk," requiring additional safeguards.

- India: The RBI's FREE-AI framework requires AI models to be explainable by design with Board-approved governance policies.

Agentic systems can satisfy these requirements through governance infrastructure built on risk-CTO-COO collaboration. This means establishing dedicated "AgentOps" functions, embedding QA and compliance agents into every AI squad, and maintaining complete auditability of every decision.

The Practical Work Split

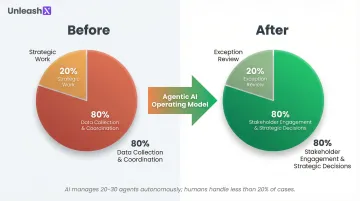

Humans move from spending 80% of time on data collection and coordination toward spending 80% on stakeholder engagement, exception review, and strategic decision-making. In an agentic operating model, employees shift to managing 20–30 AI agents, validating outputs and refining model behavior. Manual intervention is reserved for the highest-complexity exceptions less than 15–20% of total case volume while AI handles routine tasks autonomously.

Why Most Banks Get Stuck in Pilot Purgatory And How to Move Forward

Defining the Problem

75% of banks remain stuck in siloed pilots, and Gartner predicts 30% of GenAI projects will be abandoned post-POC by the end of 2025. Banks deploy narrow AI use cases, a chatbot here, a credit memo tool there to see limited ROI, and plateau because they're deploying point solutions rather than redesigning end-to-end domains. Nearly two-thirds of organizations have not begun scaling AI, and only 39% report any EBIT impact at the enterprise level.

Five Failure Modes

McKinsey identifies five primary reasons banks fail to scale AI and capture financial value:

- Functional silos: Initiatives driven within isolated business units with unclear links to financial value

- Over-reliance on Gen AI: Chasing impact from generative AI alone rather than combining it with agentic AI and automation

- Narrow point solutions: Deploying isolated tools instead of driving end-to-end transformation of business domains

- Treating LLMs like analytics: Managing large language model applications with the same limited scope as traditional predictive models

- Limited capability reuse: Failing to build cross-cutting AI capabilities, resulting in poor ROI as different divisions build redundant tools

Breaking Out: What It Takes

Moving beyond pilot purgatory requires four shifts:

- Link AI initiatives directly to financial outcomes like cost reduction targets, revenue growth, or capacity creation not just efficiency metrics

- Focus on 2-3 high-value domains like KYC, loan origination, or fraud prevention; target measurable impact within 12-18 months

- Align CEO, COO, CTO, and CRO from the start. AI transformation spans business units, technology infrastructure, and risk management simultaneously

- Deploy production-ready solutions that let you validate agentic impact fast, without building infrastructure from scratch (platforms like UnleashX go live in under 45 minutes with 200+ tool integrations and built-in compliance monitoring)

Agentic AI can drive up to 70% gross cost reductions in specific operations but the net aggregate reduction lands at 15-20% once technology investments are factored in. Banks that move decisively on the four shifts above, rather than running another isolated pilot, are best positioned to close that gap.

Frequently Asked Questions

What are some examples of agentic AI in banking and finance?

Common examples include autonomous KYC onboarding that cuts processing from 95 days to hours, real-time fraud detection with self-directed investigation workflows, AI-assisted credit assessment with automated document analysis, and compliance monitoring that gathers audit data without human prompting.

How are Indian banks like HDFC, ICICI, SBI, and Axis adopting agentic AI in banking?

Indian BFSI is among the fastest adopters of agentic AI in banking. Use cases include KYC and re-KYC automation, fraud triage, claims and underwriting, multilingual support across English, Hindi, and regional languages, and cross-sell journeys on WhatsApp. NASSCOM tracks Indian banks running these in production alongside RPA for backend ledger and compliance workflows.

What are the biggest challenges banks face when deploying agentic AI?

The most common pitfalls are siloed pilots without C-suite alignment and the tendency to chase narrow use cases rather than end-to-end workflow transformation. Regulatory validation requirements and the absence of dedicated AgentOps governance compound the problem.

What Indian regulations affect agentic AI in banking deployments in BFSI?

RBI guidelines on IT outsourcing and risk-based supervision apply broadly. DPDP 2023 governs personal data handling. IRDAI rules cover insurance flows. For UPI-linked or AA-linked workflows, RBI's account aggregator framework and NPCI guidelines apply. Production deployments must maintain audit trails, explainability for adverse actions, and data localisation per RBI's storage circular.

Is agentic AI compliant with banking regulations?

Compliance depends entirely on system design and governance. Banks must route models through model risk management review (SR 11-7, EBA, or RBI frameworks), maintain audit trails, and align controls with GDPR and internal audit protocols.

Is agentic AI in banking cost-effective for Indian SMEs and cooperative banks?

Yes. Indian SaaS pricing is usage-based and INR-denominated, so smaller co-operative banks, NBFCs, and SME-focused fintechs can deploy in modular phases. Common entry points are KYC document automation, WhatsApp customer support in Hindi or regional languages, and renewal nudges, each delivering ROI within months rather than the long deployment cycles legacy systems require.

Want to see how UnleashX AI Employees can transform your business? Visit UnleashX to explore the full platform and book a personalized demo.