Introduction

Voice-enabled AI for debt collection isn't a plug-and-play deployment. It spans telephony infrastructure, CRM architecture, and conversational AI design and every layer must align with compliance obligations (FDCPA, TCPA, GDPR) before a single outbound call goes live.

Who realistically handles this integration? In-house IT or operations teams with telephony and API experience, or dedicated implementation partners. Either way, legal or compliance team sign-off is required before go-live bypassing that review is where most regulatory exposure begins.

This guide covers the complete integration of voice AI into debt collection workflows from infrastructure prerequisites through step-by-step setup, compliance validation, and post-launch testing. The goal: help you deploy a system that recovers debt effectively while staying fully compliant.

Key Takeaways

- Voice AI debt collection integration covers telephony, CRM sync, compliance rules, and call-flow design not a single-step deployment

- Prerequisites include a compatible telephony stack (SIP/VoIP), CRM API access, and pre-defined compliance rules covering consent, opt-out, and call timing

- Deployment runs in sequence: infrastructure → AI agent setup → CRM sync → compliance guardrails → testing → go-live

- Go-live timelines range from 45 minutes using pre-built templates (like UnleashX) to several weeks for custom enterprise builds

Before You Begin: Prerequisites and System Requirements

Before integration starts, three foundational elements must be in place:

- Telephony readiness: SIP trunking or a VoIP provider (Twilio, Vonage, or an existing contact centre platform) configured and operational, supporting SIP (RFC 3261) for session management and RTP (RFC 3550) for audio delivery.

- CRM accessibility: API credentials and webhook support from your CRM. Platforms like Salesforce (Platform Events) and Microsoft Dynamics 365 (Dataverse Webhooks) provide the event-driven architecture real-time voice AI requires. Synchronous API polling creates rate limit problems at volume asynchronous webhooks are the only viable path.

- Data hygiene: Clean debtor records with valid contact numbers, accurate account status flags, and consent records. Garbage data produces garbage outcomes and compliance violations.

With those foundations confirmed, the next step is verifying your existing stack can support the integration.

Compatibility Checks

Confirm whether your existing dialler or contact centre platform supports AI agent integration via API or native connector. Legacy predictive diallers often require middleware layers or full replacement, as they were built before conversational AI workflows existed.

Integration Non-Negotiables

Do not proceed without:

- Confirmed compliance framework (jurisdiction-specific call time windows, consent records, opt-out list integration)

- Defined human escalation path for sensitive or disputed calls

- Legal or compliance team sign-off on call scripts and disclosure requirements

Tools and Systems Required

Essential:

- Telephony API or SIP connector

- CRM with webhook/API support (Salesforce, HubSpot, Zoho, Microsoft Dynamics)

- Voice AI platform with debt collection capabilities

- Secure data transfer protocol (TLS/HTTPS)

- Audit log system

Recommended:

- Sentiment analysis layer for detecting distress or escalation cues

- Call recording and transcription system

- Payment gateway integration for in-call payment capture

How to Integrate Voice AI Into Your Debt Collection Workflow

Voice AI debt collection integration follows a defined sequence: telephony connection first, then AI configuration, then CRM sync, then compliance setup, then testing. Each step depends on the one before it skipping ahead creates latency problems, data gaps, or compliance exposure.

Connecting Telephony Infrastructure

Configure your SIP trunk or VoIP provider to route outbound and inbound calls through the voice AI platform. Assign dedicated DIDs (Direct Inward Dialling numbers) for debt collection campaigns, this enables call tracking and compliance monitoring by campaign type.

Critical configurations:

- Set call routing rules and transfer logic before moving to AI configuration

- Configure failover paths (best practice: failover to next IP after 4 seconds of no response to SIP INVITE)

- Use Opus codec (RFC 7587) instead of G.711 for lower latency and better Speech-to-Text accuracy

- Implement SRTP (RFC 3711) for encrypted audio media

- Ensure DTMF handling uses RFC 4733 (out-of-band named telephony events) for reliable digit capture

Outbound campaigns must use verified Caller ID numbers. Under STIR/SHAKEN regulations, caller ID information must be authenticated to combat spoofing.

Configuring the AI Agent for Debt Collection

Build and configure the voice AI agent's conversation flow with these components:

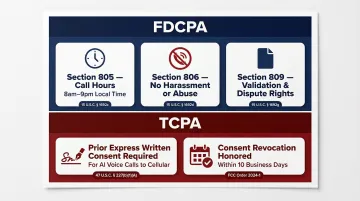

- Opening disclosure (legally required in most jurisdictions): the AI must identify itself as automated. The FCC's 2024 Declaratory Ruling (FCC 24-17) classifies AI-generated voices as "artificial or prerecorded," mandating prior express consent.

- Account verification: confirm debtor identity before discussing account details

- Balance communication: state current balance, days overdue, and payment options clearly

- Payment arrangement logic: offer payment plans, capture promises-to-pay, and record commitments

- Objection handling scripts: address common objections ("I already paid," "This isn't my debt," "I can't afford this") with compliant responses

- Escalation triggers: define conditions that immediately transfer to a human agent like disputes, financial hardship, legal threats, or emotional distress signals

Debt collection dialogue requires more careful scripting than general customer service tone, phrasing, and information disclosure are regulated. The FDCPA Section 809 requires validation information including dispute rights to be provided to consumers.

Integrating with Your CRM and Account Management System

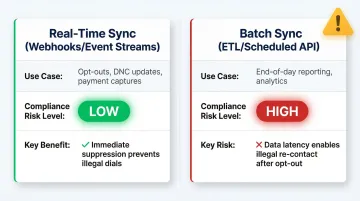

Set up bidirectional CRM sync: the AI agent must pull debtor account data (balance, days overdue, prior contact history, consent status) before each call and push call outcomes (promise-to-pay recorded, dispute flagged, payment collected) back to the CRM in real time.

Why real-time sync matters:

| Sync Method | Best Use Case | Compliance Risk | |-------------|---------------|-----------------|\n| Real-time (webhooks/event streams) | Opt-outs, DNC updates, payment captures | Low - Immediate suppression prevents illegal dials | | Batch (ETL/scheduled API) | End-of-day reporting, analytics | High - Data latency means consumers could be dialled hours after opting out |

For DNC suppression and consent revocation, real-time sync is the only safe option batch processing introduces latency that can trigger violations. Three additional considerations for high-volume deployments:

- High-volume dialers can exhaust CRM API limits (Salesforce: 1,000–100,000 calls per day depending on tier)

- Implement asynchronous processing with queuing and backpressure to handle spikes

- If a CRM lookup times out, route to a general queue rather than dropping the call

Setting Up Compliance Guardrails Within the Platform

Programme call-time restrictions, maximum call attempt limits, opt-out detection, and mandatory verbal disclosures as system-level rules not relying on the agent's conversational logic alone.

Critical compliance configurations:

Call-time restrictions:

- US (FDCPA Section 805): 8am–9pm local time at the consumer's location

- India (RBI circular RBI/2022-23/108): 8am–7pm for loan recovery calls

Maximum contact frequency:

- The CFPB presumes an FDCPA violation if a collector places a call about a debt more than seven times within seven consecutive days

Opt-out detection:

- The FCC mandates honouring do-not-call and consent revocation requests within a reasonable time, not to exceed 10 business days

Mandatory disclosures: the AI must identify itself as automated in the opening statement and provide validation information per FDCPA Section 809.

Configuring these as platform-level rules rather than scripted conversation logic means they fire regardless of call flow variation. UnleashX enforces call-time windows, opt-out suppression, and IRDAI/GDPR audit trails at the system level, so compliance isn't dependent on how a specific conversation unfolds.

Connecting Payment Processing (If Applicable)

Link a payment gateway so debtors can make payments during the call via DTMF (keypad input) or via a post-call payment link sent via SMS.

PCI-DSS compliance considerations:

Capturing payments via DTMF during an AI call brings the telephony environment into PCI-DSS scope unless strict DTMF masking/suppression is deployed. PCI-DSS v4.0.1 Requirement 3.3.1 strictly prohibits storing Sensitive Authentication Data (SAD) including full track data, CVV, and PIN after authorisation.

Recommended approach: Shift to post-call SMS payment links to remove the telephony stack from PCI scope. This keeps the telephony infrastructure entirely out of scope and shifts compliance burden to an SAQ A (e-commerce) environment.

If in-call DTMF payment capture is required, implement network-level DTMF suppression that replaces tones with flat or random sounds before they reach the agent or call recording system.

Compliance and Regulatory Requirements for Voice AI Debt Collection

Voice AI debt collection operates under a patchwork of jurisdiction-specific laws. This section covers the core requirements across India, Europe/UK, and the international jurisdictions UnleashX customers most often operate in — the three regulatory environments most deployment teams will encounter.

India: RBI Fair Practices Code and TRAI Regulations

RBI Master Direction — Recovery Agents (NBFCs and Banks):

- Time-of-contact restrictions: Calls and visits permitted only between 7am and 7pm local time, with no contact at the borrower's workplace except in specific cases

- Anti-harassment provisions: Prohibit abuse, threats, or false representation. Recovery agents must be on the lender's approved registered list and must clearly identify themselves

- Dispute and validation rights: Borrowers retain the right to dispute liability; lenders must provide loan and dues statements on request

TRAI's UCC and TCCCPR Regulations:

The TRAI Telecom Commercial Communications Customer Preference Regulations, 2018 cover commercial voice calls including AI-driven debt-collection outreach. This means:

- DLT registration on a TRAI-approved blockchain platform is mandatory for sender headers

- Prior consent from the borrower is required (typically captured at loan agreement signing); revocation must be honoured within seven days

- All calls must originate from registered numeric sender IDs; voice-content templates must be pre-registered

Europe/UK: GDPR and FCA

GDPR Article 22 restricts organizations from making solely automated decisions, including profiling, that have a legal or similarly significant effect on individuals. This is only permitted if:

- Necessary for a contract

- Authorised by law

- Based on the individual's explicit consent

Organizations must provide meaningful information about the logic involved and allow consumers to obtain human intervention.

FCA (Financial Conduct Authority): CONC 7.9 requires that anyone contacting a customer on a firm's behalf clearly explains the purpose of the contact.

India: RBI Guidelines

The August 2022 RBI circular (RBI/2022-23/108) strictly prohibits recovery agents from resorting to intimidation or harassment. It explicitly restricts calling borrowers before 8am and after 7pm for the recovery of overdue loans.

Consent Management and Disclosure Requirements

Consent verification: Configure prior written consent verification before outbound AI calls. Handle revocation of consent in real time immediate suppression, no re-contact until re-consent is obtained.

AI disclosure: The AI agent must identify itself as automated in the opening statement in most jurisdictions. "Passing as human" is a legal and reputational risk. The FCC's August 2024 NPRM (FCC 24-84) proposes requiring callers using AI-generated voice to clearly disclose this at the beginning of the call.

Audit and record-keeping: All AI-driven debt collection calls must be logged with timestamps, call recordings (where legally permitted), call outcomes, and any promises-to-pay or disputes raised. This logging must be automated and tamper-proof for regulatory audit purposes. Getting this infrastructure right before go-live is far easier than retrofitting it after a compliance audit.

Post-Integration Testing and Validation

Validation must happen before any live debtor contacts. A misconfigured compliance rule or broken CRM sync discovered after launch can trigger regulatory complaints and corrupt account records across every affected account.

Functional Call Testing

Run end-to-end test calls through each script branch:

- Successful payment arrangement

- Disputed debt

- Unresponsive debtor

- Escalation to human agent

Latency benchmarks: Human conversational gaps average 200 milliseconds. For conversational AI to feel natural, end-to-end latency must stay under one second. Industry data shows that latency under 1 second yields ~5% abandonment, while 2-3 seconds causes abandonment to spike to ~15%.

Confirm that DTMF inputs are correctly detected, call transfers execute cleanly, and response times stay within acceptable thresholds. Once call-level behavior is confirmed, the next step is verifying that every outcome has been written back to your CRM correctly.

CRM Sync Validation

After test calls, audit CRM records manually to confirm all call outcomes have been captured:

- Promise-to-pay dates

- Dispute flags

- Payment confirmations

- Failed or dropped calls logged with accurate status codes

Check that no data is left as blanks or "pending" indefinitely.

Compliance Configuration Audit

Before go-live, run a compliance checklist:

- ✅ Call-time restrictions active and enforced

- ✅ Opt-out suppression functioning in real time

- ✅ Disclosure scripts playing correctly

- ✅ Maximum contact frequency limits enforced

- ✅ Time zone handling configured to local consumer time (not UTC)

Involve your legal or compliance team in formal sign-off before any live contacts begin.

Common Integration Problems and How to Fix Them

Most voice AI integration failures trace back to a small set of recurring issues misconfigured timeouts, latency bottlenecks, and compliance sync gaps. Here's how to diagnose and fix each one.

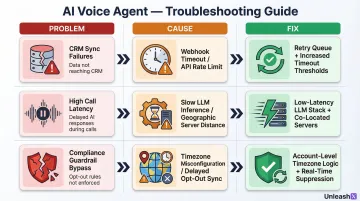

CRM Sync Failures or Delayed Data Writes

Problem: Call outcomes are not appearing in the CRM, or data is writing with significant delay, causing agents to re-contact debtors who have already made arrangements.

Likely cause: Webhook timeout settings are too short, or the CRM API rate limit is being hit during high-volume campaign runs.

Fix:

- Increase webhook timeout thresholds (5-10 seconds recommended)

- Implement a retry queue for failed writes

- Review CRM API rate limits consider batching low-priority updates during off-peak hours

High Call Latency or Unnatural Pauses in Conversation

Problem: Debtors are hanging up due to robotic-sounding pauses between their responses and the AI's reply, resulting in low contact-to-resolution rates.

Likely cause: Slow LLM inference times or high network latency between telephony provider and AI platform; often worsened by overly long context windows in the AI configuration.

Fix:

- Optimise the AI agent's context length

- Switch to a low-latency LLM stack

- Ensure telephony and AI platform servers are in the same geographic region

- Target sub-700ms response latency for natural-sounding voice AI

Compliance Guardrail Bypass Due to Misconfiguration

Problem: Calls are being placed outside permitted hours, or debtors on opt-out lists are being contacted creating regulatory exposure.

Likely cause: Time zone handling errors (local time vs. UTC misconfiguration) or opt-out list sync running on a delayed schedule rather than in real time.

Fix:

- Enforce time zone localisation at the account level (not campaign level)

- Switch opt-out suppression to real-time sync triggered immediately upon opt-out capture

- Run daily automated compliance audits against call logs

- Hardcode local-time validation logic using area code and postal code mapping directly into the AI dialler's pre-call routing rules

Pro Tips for a Successful Voice AI Debt Collection Integration

Start with a Pilot Campaign

Start with a limited pilot campaign on a low-risk debtor segment early-stage accounts, lower balances before deploying across the full portfolio. This surfaces configuration issues with minimal regulatory or financial risk.

Design Human Escalation Logic Carefully

Define specific triggers that immediately transfer the call to a live agent. Common escalation points include:

- Debtor disputes or account challenges

- Mentions of financial hardship or vulnerability

- Legal threats or attorney references

- Distress signals and emotional cues

Over-relying on AI for complex situations is where most deployment failures occur in debt collection.

Document Everything Before Go-Live

Maintain a configuration record that captures your AI agent script versions, compliance rule settings, CRM field mappings, and telephony routing logic. This documentation is essential for audit defense and simplifies future updates or platform migrations.

Conclusion

The quality of a voice AI debt collection integration is determined in the setup phase. Compliance configuration and CRM sync architecture matter far more than the AI model itself. A well-integrated system that handles disclosures, escalations, and data writes correctly will consistently outperform a more sophisticated AI running on a poorly configured stack.

McKinsey research projects that generative AI in debt collection can slash operational costs by 40% and increase debt recoveries by 10% through improved first-contact resolution and data-driven calling decisions.

Sustaining those results requires treating this as an ongoing system, not a one-time deployment. Keeping the integration performing means revisiting:

- Call scripts as debtor behavior patterns shift

- Compliance rules as regulations evolve

- Escalation triggers whenever edge cases surface in call data

The FCC's 2024 rulings on AI voices confirm that compliance requirements will continue to tighten teams that build review cycles into their process now will be better positioned when the next rule change arrives.

Frequently Asked Questions

How does AI fit Indian mortgage lenders, HFCs, and NBFCs?

Indian housing finance companies (HDFC Ltd, LIC HF, PNB HF) and NBFCs use AI for application triage, document verification (Aadhaar / PAN / income proofs), property valuation analytics, and customer follow-up across English, Hindi, and regional languages. RBI and NHB guidelines on IT outsourcing govern deployments, so providers maintain audit trails for every decision.

What compliance regulations must voice AI debt collection systems follow?

Key frameworks: RBI Fair Practices Code, TRAI TCCCPR 2018, and the DPDP Act 2023 in India, with GDPR and FCA guidelines covering Europe. The AI system itself must enforce these rules programmatically through system-level guardrails not rely on agent discretion.

Which Indian regulations apply to AI in mortgage and home loan workflows?

RBI master directions for HFCs and NBFCs, NHB regulations, DPDP 2023 for personal data, and IT Act provisions on electronic records all apply. KYC for housing loans is governed by RBI's master KYC direction and CKYC. Production AI systems for lending must keep model decision logs, fair-lending audit trails, and adverse-action reasons retrievable on demand.

How do Indian borrowers prefer to interact with mortgage lenders?

WhatsApp and voice calls dominate Indian borrower engagement. SMS-based status updates, regional-language voice IVRs, and human handoff inside the same WhatsApp thread are standard expectations. Lenders combining voice AI for first-touch with branch RM follow-up see higher application completion rates compared with email-led journeys typical in Western markets.

What happens if a debtor disputes a debt during an AI call?

The AI should immediately acknowledge the dispute, cease collection activity on that account, and log the dispute flag to the CRM in real time. It should then transfer the call to a human agent or schedule a callback, in line with FDCPA dispute handling requirements.

How do you measure the success of a voice AI debt collection integration?

Key metrics: right-party contact rate, promise-to-pay rate, payment conversion rate, compliance incident rate (target: zero), average handling time, and CRM data accuracy post-call. Track these weekly during the first 90 days post-launch to identify issues early.

Want to see how UnleashX AI Employees can transform your business? Visit UnleashX to explore the full platform and book a personalized demo.