Introduction

Underwriting decisions that once took days or weeks are now a competitive liability. Applicants expect near-instant responses, and delays directly translate to lost policies and abandoned loan applications. Traditional mortgage underwriting averages 51 to 58 days, while life insurance underwriting takes 28 days on average. During these waiting periods, qualified applicants shop competing offers and many don't return.

AI agents autonomous, multi-step systems that reason and execute across multiple data sources do something rule-based automation cannot: they handle unstructured data, adapt to exceptions, and complete multi-step workflows without human handoffs at each stage. That capability directly targets where underwriting slows down.

This article covers:

- Where underwriting delays actually originate

- How AI agents resolve each bottleneck

- Sector-specific applications in banking and insurance

- What responsible deployment looks like

Key Takeaways

- Underwriting delays stem from a chain of manual steps like data gathering, document review, verification, and coordination across multiple stakeholders

- AI agents differ from basic automation by autonomously orchestrating multi-step workflows across systems, not just executing single, pre-programmed tasks

- AI agents cut time-to-decision in banking and insurance by running data prefill, document analysis, risk scoring, and applicant follow-up in parallel

- Human underwriters stay focused on complex decisions; AI agents clear the high-volume groundwork that builds backlogs

Why Underwriting Delays Are More Costly Than They Appear

The Compounding Delay Chain

Underwriting isn't a single decision, it's a sequence of dependent tasks. Application intake waits on data gathering. Document verification waits on intake completion. Risk scoring waits on verification. Approval routing waits on scoring. A one-day lag at each of five stages creates a week-long queue, even for straightforward applications.

This compounding effect means simple cases get trapped behind complex ones. Qualified applicants wait unnecessarily while underwriters chase missing documents instead of analyzing risk.

The Revenue Cost of Slow Decisions

Improving mortgage application completion rates from 70% to 80% generates 137 additional funded loans and $1.23 million (approximately ₹10.2 crore) in additional gross revenue per 10,000 application starts. Every day an applicant waits is another day they can accept a competitor's offer.

In life insurance, 59% of individual life applications are eligible for accelerated underwriting, yet many insurers still route them through full medical review processes. The opportunity cost is measurable: companies using accelerated workflows see an average improvement of 19 business days from application submission to final decision.

The Administrative Tax on Underwriters

Underwriters spend 40% of their time on administrative tasks, including chasing documents, manually re-keying form data, and coordinating with third-party providers. Only 30% of their time goes to actual underwriting and risk analysis.

This misallocation creates compounding problems across the pipeline:

- High-value underwriter time is consumed by low-value administrative tasks

- Application queues grow as senior underwriters can't focus on genuinely complex cases

- Error rates climb when backlogs force rushed reviews on cases that deserved closer scrutiny

Premium Leakage and Mispricing Risk

These time costs don't stay contained to operations, they reach the balance sheet. Risk profiles shift between application and final decision, and in commercial property insurance, delayed physical inspections routinely produce mispriced policies. Premium audits then uncover undisclosed business activities or operational changes that occurred during extended underwriting periods, triggering premium leakage and loss ratio deterioration.

In volatile lines like health insurance and commercial property, static point-in-time data ages fast. The longer a decision takes, the wider the gap between the risk assessed and the risk actually being priced.

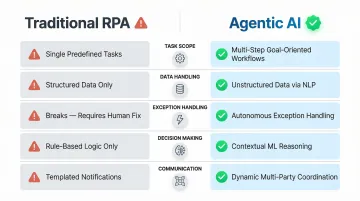

AI Agents vs. Basic Automation: What's the Difference?

Where Rule-Based RPA Falls Short

Robotic Process Automation (RPA) excels at single, predictable tasks within rigid workflows extracting a field from a structured form, copying data between systems, sending templated emails. But RPA breaks down when:

- Data is missing or incomplete

- Documents arrive in unstructured formats

- Contextual judgment is required

- Exceptions need autonomous handling

Most real underwriting scenarios involve all four conditions. A mortgage application might include handwritten bank statements, incomplete employment records, and property appraisals in PDF format. RPA can't navigate this complexity without constant human intervention.

What Makes AI Agents Different

Agentic AI systems are goal-oriented. They decompose multi-step objectives, decide which tools or data sources to use at each step, handle exceptions autonomously, and coordinate with external parties. Unlike RPA scripts, they adapt when inputs change mid-process.

Key distinctions:

| Capability | Traditional RPA | Agentic AI |

|---|---|---|

| Task Scope | Single, predefined tasks | Multi-step, goal-oriented workflows |

| Data Handling | Structured formats only | Unstructured documents via NLP |

| Exception Handling | Breaks and requires human fix | Autonomous problem-solving |

| Decision Making | Rule-based logic only | Contextual reasoning with ML models |

| Communication | Templated notifications | Dynamic, multi-party coordination |

Multi-Agent Architecture in Practice

McKinsey describes a future where underwriting is delivered through AI multi-agent systems acting as virtual coworkers. Specialized agents work in parallel:

- Intake Agent: Ingests documents, extracts data from unstructured formats, and communicates directly with applicants

- Risk Profiling Agent: Builds risk profiles by cross-referencing applicant data against underwriting guidelines and historical patterns

- Pricing Agent: Calculates premiums and recommends policy structures based on the risk profile

- Compliance Agent: Flags regulatory gaps and verifies adherence to internal audit standards

- Decision Orchestrator: Aggregates all agent outputs to trigger auto-approval or route edge cases to a human reviewer

This parallel execution compresses what was a sequential manual process. Instead of five stages running one after another, specialized agents work simultaneously cutting total cycle time from days to hours.

How AI Agents Eliminate Underwriting Bottlenecks

Automated Data Collection and Prefill

AI agents pull applicant data from credit bureaus, public property records, claims histories, medical information bureaus, and third-party risk databases autonomously. They eliminate the back-and-forth between underwriters, agents, and applicants that typically adds days to intake.

In life insurance, Electronic Health Record (EHR) retrieval speeds up underwriting from 15 days to just 2 days. Rather than waiting weeks for Attending Physician Statements, AI agents retrieve medical records electronically and synthesize findings into structured risk profiles.

Platforms like UnleashX deploy full-stack AI employees with cross-system synchronization across CRMs and external APIs operating 24/7 with under 700ms response latency and 98% accuracy, without any human scheduling.

Unstructured Document Processing via NLP

Traditional RPA completely fails when documents lack standardized formats. AI agents read and extract key data from medical records, loss run reports, financial statements, and engineering surveys turning hours of manual review into seconds of structured output.

John Hancock uses Munich Re's alitheia platform, which applies natural language processing to categorize free-form text responses in EHRs and assess mortality risk. The result: most applications reach a decision within two days rather than two weeks.

Real-Time Risk Scoring and Dynamic Model Updates

That structured data from document processing feeds directly into machine learning models, which continuously evaluate it against historical claims patterns, environmental risk factors, and behavioral signals. Instead of a static score calculated once at manual review, AI agents produce dynamic risk scores that update as new information arrives.

According to hyperexponential's analysis of agentic AI in underwriting, commercial P&C insurers using AI achieve 3-5% loss ratio improvements and 60-99% faster quote turnaround. These gains come from identifying risk patterns human underwriters miss and updating pricing models in real time.

Multi-Party Communication Orchestration

AI agents autonomously manage the full coordination loop that typically creates the longest delays:

- Send follow-up requests to applicants for missing documents

- Communicate directly with medical providers or property inspectors

- Push status updates to brokers across voice, chat, and email

- Log every interaction into the CRM without manual input

This runs continuously, no applicant waits for business hours, and no follow-up falls through the cracks.

Intelligent Triage and Escalation Routing

AI agents auto-approve straightforward low-risk applications immediately and flag only genuinely complex or high-value cases for human underwriter review. Gen Re's 2025 survey shows 12% of applications are eligible for fully automated decisioning, with 47% eligible for accelerated underwriting with human review.

This triage ensures senior underwriters concentrate their time where judgment is actually needed rather than diffused across the entire application queue. Of applications sent through automated workflows, 86% are ultimately placed demonstrating that intelligent routing doesn't sacrifice approval rates.

Banking Loan Underwriting vs. Insurance: Specific Applications

Banking and Mortgage Lending

AI agents accelerate loan underwriting by automating income verification, credit analysis, debt-to-income calculations, and property valuation data retrieval. Lenders using Freddie Mac's digital capabilities save an average of ₹1.4 lakh (≈ $1,700)per loan and shorten production timelines by 5 days.

How AI agents handle borrower financial analysis:

- Pull from bank statements, tax records, and employment databases simultaneously

- Validate income documentation against third-party verification sources

- Calculate debt-to-income ratios automatically with real-time data

- Flag discrepancies or missing information for human review

Fannie Mae's Desktop Underwriter validation services have helped lenders cut as much as 11.9 days off their application-to-close time by providing "Day 1 Certainty" immediate validation that loans meet eligibility requirements.

Property and Casualty Insurance

Where banking underwriting relies on financial records, P&C insurance hinges on physical property assessment. AI agents close that gap by enabling virtual property surveys using satellite imagery and drone footage, removing the scheduling delay of physical inspections. Verisk's Aerial Imagery Analytics provides coverage of 99.6% of U.S. structures, using computer vision to assess visible roof defects automatically.

CAPE Analytics' Roof Condition Rating model visualizes and quantifies roof issues directly on high-resolution imagery, allowing carriers to maintain rate adequacy and increase market share without dispatching inspectors.

AI agents also ingest real-time climate and environmental data to update property risk profiles dynamically. This ensures pricing reflects current conditions rather than outdated assumptions, reducing mispricing risk in volatile property markets.

Life and Health Insurance

Life insurance underwriting historically involved weeks of waiting for medical information. AI agents expedite this by communicating directly with medical providers, parsing records via NLP, and synthesizing findings into structured risk profiles.

Companies using accelerated underwriting workflows see average improvements of 19 business days from application submission to final decision compared to full underwriting workflows. Applicants who receive decisions in days rather than weeks are measurably more likely to accept offers, a direct conversion advantage for carriers that invest in automation.

Compliance, Fairness, and the Human Underwriter's Evolving Role

Bias and Fairness: Non-Negotiable Requirements

AI models trained on historical data can perpetuate discriminatory patterns if not actively audited. Responsible deployment requires:

- Regular algorithmic audits to detect bias in decision patterns

- Diverse training data that represents full applicant populations

- Transparent decision rationale that human underwriters can review and override

The NAIC's 2024 Model Bulletin on AI Systems requires insurers to develop written programs to mitigate the risk of Adverse Consumer Outcomes, including governance, risk management controls, and internal audit functions.

Regulatory Compliance Automation

AI agents can be configured to enforce compliance rules in real time checking that every decision aligns with applicable frameworks like NAIC guidelines, GDPR, and internal audit protocols. They maintain a full audit trail of every data point accessed and every decision step taken.

Key regulatory frameworks:

| Framework | Issuing Body | Core Requirements |

|---|---|---|

| AI Systems Model Bulletin | NAIC (2024) | Written AIS Program to mitigate Adverse Consumer Outcomes with governance and audit functions |

| AVM Final Rule | CFPB/Interagency (2024) | Quality control standards for Automated Valuation Models ensuring nondiscrimination compliance |

| GDPR Article 22 | EU (2016) | Measures to allow audits and inspections of automated processing |

UnleashX's AI employees are built to enforce these requirements in practice logging every decision step, flagging rule violations in real time, and supporting human review before final decisions are issued. The Human-in-the-Loop model means compliance oversight doesn't require separate manual review workflows.

The Evolving Role of Underwriters

Robust compliance infrastructure changes what underwriters spend their time on. AI agents absorb the data gathering, document chasing, and rule-checking shifting the underwriter's role toward strategic risk judgment and client relationships. Early adopters are already reporting improvements in underwriting accuracy and loss ratios as a result.

What changes:

- Less time chasing documents and re-keying data

- More time on complex risk judgment requiring institutional knowledge

- Greater focus on client relationships and strategic decisions

- Expanded capacity to handle high-value, nuanced cases

In life insurance, managing mortality slippage remains a human responsibility. 66% of companies estimate mortality slippage between 6% and 15% when bypassing fluids and exams. To manage this, 86% use or plan to implement pre-/post-issue auditing with random holdouts as control measures work that requires human oversight.

Frequently Asked Questions

What is the automated underwriting system?

An automated underwriting system (AUS) evaluates insurance or loan applications against predefined risk criteria, returning an automated decision like approve, refer, or decline without full manual review. AI agents extend this further by handling unstructured data and complex multi-step reasoning that basic rule engines cannot.

How are Indian banks like HDFC, ICICI, SBI, and Axis adopting agentic AI in banking?

Indian BFSI is among the fastest adopters of agentic AI in banking. Use cases include KYC and re-KYC automation, fraud triage, claims and underwriting, multilingual support across English, Hindi, and regional languages, and cross-sell journeys on WhatsApp. NASSCOM tracks Indian banks running these in production alongside RPA for backend ledger and compliance workflows.

How does AI improve underwriting in the insurance industry?

AI improves insurance underwriting by automating data collection, enabling real-time risk scoring, and processing unstructured documents through natural language processing. This reduces time-to-decision and improves pricing accuracy by surfacing risk patterns that manual review tends to miss.

What Indian regulations affect agentic AI in banking deployments in BFSI?

RBI guidelines on IT outsourcing and risk-based supervision apply broadly. DPDP 2023 governs personal data handling. IRDAI rules cover insurance flows. For UPI-linked or AA-linked workflows, RBI's account aggregator framework and NPCI guidelines apply. Production deployments must maintain audit trails, explainability for adverse actions, and data localisation per RBI's storage circular.

Is agentic AI in banking cost-effective for Indian SMEs and cooperative banks?

Yes. Indian SaaS pricing is usage-based and INR-denominated, so smaller co-operative banks, NBFCs, and SME-focused fintechs can deploy in modular phases. Common entry points are KYC document automation, WhatsApp customer support in Hindi or regional languages, and renewal nudges, each delivering ROI within months rather than the long deployment cycles legacy systems require.

What are the 4 types of underwriting?

The four main types are insurance underwriting, loan/mortgage underwriting, securities underwriting, and forensic underwriting. AI agents are currently having the most immediate impact on insurance and loan underwriting due to the high volume of data-intensive, repeatable decisions involved.

Want to see how UnleashX AI Employees can transform your business? Visit UnleashX to explore the full platform and book a personalized demo.