Introduction

Banks and financial institutions are under mounting pressure: call volumes are climbing, customers expect instant resolution at any hour, and round-the-clock human staffing costs keep rising. In 2023, average call durations reached 442 seconds (over seven minutes per interaction), while contact center attrition hit 31% annually.

That attrition forces institutions to absorb turnover costs ranging from ₹15.4 lakh (≈ $18,500)to ₹61.4 lakh (≈ $74,000)per agent, a recurring drain that legacy support models weren't built to handle.

Voice AI is already delivering measurable results across daily operational metrics: reduced wait times, improved first-call resolution, lower cost per interaction, and consistent compliance adherence. This article covers what Voice AI actually does for banking operations today.

Key Takeaways

- Voice AI handles customer queries 24/7 without proportionally scaling human headcount

- Reduces cost per interaction from ₹598 (≈ $7.20)–₹996 (≈ $12.00)to ₹25 (≈ $0.30)–₹42 (≈ $0.50)while cutting average handle time by 30–50%

- Delivers 100% compliance monitoring with complete audit trails, addressing vulnerabilities where manual QA reviews only 1–2% of calls

- Banks delaying adoption face compounding disadvantages: higher costs, slower service, and customer attrition to faster competitors

- Value compounds continuously but only when deployed as a persistent operational capability, not a one-off project

What Is Voice AI in Banking?

Voice AI is a system that uses natural language processing and speech recognition to understand customer requests and respond accurately without a human agent on the line. Unlike traditional IVR menus that force customers through rigid button-press options, Voice AI reads intent from natural speech "I need to block my card" or "What's my account balance?" then either resolves the query autonomously or routes it to the right place.

In banking, Voice AI handles a wide range of interactions:

- Inbound customer support and general account queries

- Fraud alert callbacks and suspicious activity verification

- Loan inquiry handling and eligibility screening

- Card blocking requests and account balance checks

- Authentication workflows before connecting to a human agent

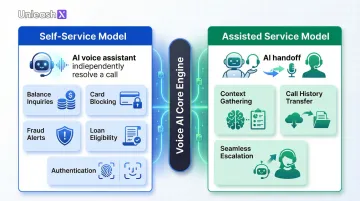

These applications fall into two models: self-service (AI resolves the issue entirely) and assisted service (AI gathers context, then hands off to a human with full call history).

The right way to evaluate Voice AI is by outcomes, not features. Banks that deploy it well see measurable gains in service availability, resolution speed, compliance risk reduction, and customer retention not because AI is novel, but because it removes the operational ceiling that human-staffed call centers hit every night, weekend, and peak season.

Key Advantages of Voice AI for Banking Customer Support

The advantages below map directly to operational outcomes banking leaders track: support cost per interaction, service availability, resolution speed, compliance risk, and customer retention. Each one compounds when Voice AI is connected to live banking systems.

Always-On Availability Without Linear Cost Increases

Voice AI enables a bank to support customers at 2 AM on a Sunday at the same cost and quality as a Tuesday afternoon something a human-staffed contact center structurally cannot do. The AI handles inbound calls simultaneously across any volume, maintains consistent response quality, and never experiences fatigue or staffing gaps during peak periods or holidays.

- AI responds to unlimited concurrent calls without queue wait times

- No shift premiums, overtime costs, or emergency hiring during demand spikes

- Consistent service quality regardless of time, day, or call volume

- Instant answer speeds (under 1 second vs. 45–90 seconds for human agents)

Research shows that Voice AI reduces after-hours abandonment rates by 91–97%, dropping from 20–35% to just 1–2%. When customers can't reach support at critical moments fraud alerts, payment failures, card blocking requests, they don't just wait. According to J.D. Power's 2024 Retail Banking Satisfaction Study, 13% of retail bank customers say they will likely switch institutions within 12 months, with 26% citing poor service as the primary reason.

Scaling human coverage for 24/7 operations requires shift premiums, redundancy hiring, and management overhead. The average fully loaded cost of a human-handled call reaches ₹996 (≈ $12), whereas an AI agent handles the same inquiry for ₹25 (≈ $0.30)–₹42 (≈ $0.50), a 95% cost reduction.

KPIs impacted:

- Service availability rate

- After-hours resolution rate

- Customer abandonment rate

- Cost per interaction

- CSAT scores for time-sensitive queries

Best fit: High-volume retail banking, digital-first banks with no physical branches, banks operating across time zones, and institutions with large bases of mobile-first customers who expect instant service at any hour.

Faster Resolution Through Intelligent Call Handling

Voice AI moves beyond static IVR menus, it understands intent in natural language, routes the customer immediately, or resolves the query autonomously without any transfer. A customer says "block my card," and the AI verifies identity via voice biometrics, executes the block, and confirms all in one conversation, in under two minutes, with no agent involved.

- Natural language understanding eliminates menu navigation

- Voice biometrics verify identity in the background, saving 45 seconds compared to manual knowledge-based authentication

- Instant data retrieval eliminates hold time entirely

- Automated summarization reduces after-call work by 60–80%

Voice AI reduces Average Handle Time (AHT) by 30–50% and improves First-Call Resolution (FCR) by 12–20 percentage points, raising rates from 70–75% to 82–90%. In financial services, delayed resolution on urgent issues like fraud, card blocks, failed transfers has an outsized impact on customer loyalty. Faster resolution on high-stakes calls is one of the strongest drivers of retention in retail banking.

HSBC UK's Voice ID system provides a concrete example: it prevented £249 million in attempted telephone fraud in a single year, reducing reported telephone banking fraud by 50% year-over-year. Voice biometrics authenticate faster than knowledge-based methods while simultaneously closing one of the most exploited fraud vectors in telephone banking.

KPIs impacted:

- Average handle time (AHT)

- First-call resolution (FCR) rate

- Call transfer rate

- Agent utilization rate

- Net Promoter Score (NPS) for support interactions

When this matters most: Institutions with high inbound call volumes, banks handling time-sensitive queries like fraud alerts or payment failures, and customer service operations where agent capacity is regularly stretched during peak periods.

Compliance-Ready Operations and Consistent Audit Trails

Every Voice AI interaction is recorded, transcribed, and logged by default creating a consistent, auditable record that human call center operations rarely achieve at scale. Voice AI systems can be configured to follow regulatory scripts precisely on every call (mandatory disclosures, consent capture, KYC verification steps), with zero deviation, unlike human agents who may skip or abbreviate steps under pressure.

- 100% of conversations are automatically scored against compliance rubrics

- Mandatory disclosures are delivered consistently without exception

- Voice biometrics provide secure, auditable identity verification

- Complete transcripts and recordings are retained for regulatory review

Most contact centers review only 1–2% of conversations through manual sampling, leaving significant monitoring gaps. In August 2024, the SEC charged 26 broker-dealers and investment advisers for recordkeeping failures, resulting in combined penalties of $392.75 million (approximately ₹3259.8 crore).

That same year, the CFTC fined a firm ₹5.4 crore (≈ $650,000) for failing to retain approximately 3,000 audio recordings of customer calls.

Voice AI eliminates this vulnerability by automatically monitoring 100% of interactions. UnleashX's AI employees support GDPR and IRDAI compliance frameworks with human-in-the-loop oversight built in so automated monitoring is paired with human review at the points that carry the most regulatory risk.

KPIs impacted:

- Compliance adherence rate

- Percentage of interactions reviewed

- Fraud detection rate

- Audit readiness score

- Cost of compliance per interaction

When this matters most: Banks operating across multiple regulatory jurisdictions, institutions undergoing digital transformation audits, and financial services firms where call center compliance has historically been a vulnerability.

What Happens When Voice AI Is Missing or Ignored

Relying solely on human agents for 24/7 banking support creates compounding costs: shift premiums, attrition (31% annually), inconsistent service quality, and an inability to scale during demand spikes without emergency hiring. The median annual wage for customer service representatives is ₹41.1 lakh (≈ $49,500), with turnover costs reaching ₹15.4 lakh (≈ $18,500)–₹61.4 lakh (≈ $74,000)per employee.

Downstream risks compound quickly:

- Customer attrition accelerates: J.D. Power found that 20% of retail bank customers moved money away from their primary bank within a three-month period in 2026, up from 17% the previous year and 26% of likely switchers cite service friction as the primary reason.

- Compliance exposure widens: Missed disclosures, undocumented conversations, and inconsistent authentication create audit vulnerabilities. Manual QA sampling covers just 1–2% of calls, leaving institutions exposed to regulatory penalties that now routinely exceed hundreds of millions of dollars.

- The competitive gap becomes structural: Bank of America's Erica handled nearly 700 million interactions in 2025 alone, surpassing 3.2 billion total since launch. Banks that deploy Voice AI early define the service benchmark and late adopters find that benchmark increasingly difficult to match.

How to Get the Most Value from Voice AI in Banking

Voice AI delivers the highest ROI when applied consistently across all customer-facing call flows not just deployed as a narrow FAQ bot for one use case. Value compounds when the system connects to live banking infrastructure: real-time account data, authentication systems, CRM platforms, and fraud detection tools. That integration is what allows the AI to act, not just respond.

Integration drives ROI:

UnleashX's AI employees are built to sync across CRMs, APIs, and external platforms natively, with go-live achievable in under 45 minutes using pre-built templates. Integrated Voice AI deployments in financial services achieve full payback within 3 to 6 months, delivering 148–200% ROI in the first year. Conversely, siloed chatbots frequently never reach positive ROI.

Track outcomes on a regular cycle:

Monitor AHT, FCR, after-hours resolution rate, and compliance adherence metrics to ensure the deployment keeps improving rather than stagnating. Benchmark self-service containment rates (20–60% depending on maturity), average handle time (4–7 minutes for general service), and first-call resolution (70–85% industry benchmark).

Start with high-impact use cases:

- Fraud alert callbacks – Real-time verification via voice biometrics

- Card blocking requests – Instant identity verification and execution

- Balance and transaction inquiries – Self-service resolution without agent involvement

- Loan inquiry handling – Eligibility checking, document collection, status updates

- Payment reminders – Proactive EMI and billing notifications across voice, WhatsApp, and SMS

These use cases cut costs, reduce call volume, and free human agents to focus on complex or relationship-intensive work.

Conclusion

Voice AI delivers compounding returns in banking across three dimensions that matter most: availability that scales without proportional cost, faster call resolution with consistent accuracy, and compliance that doesn't depend on human memory. Each dimension reinforces the others over time.

These aren't isolated wins. A system that's always on, resolves faster, and logs every interaction automatically becomes more valuable as call volume grows not less.

Banks that move from pilot to production integrating Voice AI into core infrastructure rather than running it as a side experiment are the ones pulling ahead on customer experience. The key shift is treating adoption as an operational practice: measure resolution rates, refine escalation logic, expand coverage incrementally. That's what separates lasting impact from a one-time rollout.

For Indian businesses operating across BFSI, IT services, real estate, insurance, and BFSI workflows, the same pattern applies: multilingual coverage across English, Hindi, and regional languages, WhatsApp-first customer engagement, and compliance with RBI, IRDAI, and DPDP 2023 requirements together determine production-grade success.

Frequently Asked Questions

How are Indian banks like HDFC, ICICI, SBI, and Axis adopting agentic AI in banking?

Indian BFSI is among the fastest adopters of agentic AI in banking. Use cases include KYC and re-KYC automation, fraud triage, claims and underwriting, multilingual support across English, Hindi, and regional languages, and cross-sell journeys on WhatsApp. NASSCOM tracks Indian banks running these in production alongside RPA for backend ledger and compliance workflows.

What are the common applications of AI in banking?

Key use cases include intelligent call routing, voice-based identity verification, balance and transaction inquiries, card blocking, fraud alerts, and loan inquiry handling. These span both self-service models (where AI resolves the issue entirely) and assisted service models (where AI gathers context before escalating).

Is Voice AI in banking secure and compliant with regulations?

Enterprise-grade Voice AI platforms are built to meet frameworks like PCI DSS, SOC 2, GDPR, and IRDAI. Features like voice biometrics, encrypted call logs, and human-in-the-loop oversight add layers of security and audit readiness, with 100% of interactions monitored for compliance adherence.

What Indian regulations affect agentic AI in banking deployments in BFSI?

RBI guidelines on IT outsourcing and risk-based supervision apply broadly. DPDP 2023 governs personal data handling. IRDAI rules cover insurance flows. For UPI-linked or AA-linked workflows, RBI's account aggregator framework and NPCI guidelines apply. Production deployments must maintain audit trails, explainability for adverse actions, and data localisation per RBI's storage circular.

Is agentic AI in banking cost-effective for Indian SMEs and cooperative banks?

Yes. Indian SaaS pricing is usage-based and INR-denominated, so smaller co-operative banks, NBFCs, and SME-focused fintechs can deploy in modular phases. Common entry points are KYC document automation, WhatsApp customer support in Hindi or regional languages, and renewal nudges, each delivering ROI within months rather than the long deployment cycles legacy systems require.

Want to see how UnleashX AI Employees can transform your business? Visit UnleashX to explore the full platform and book a personalized demo.